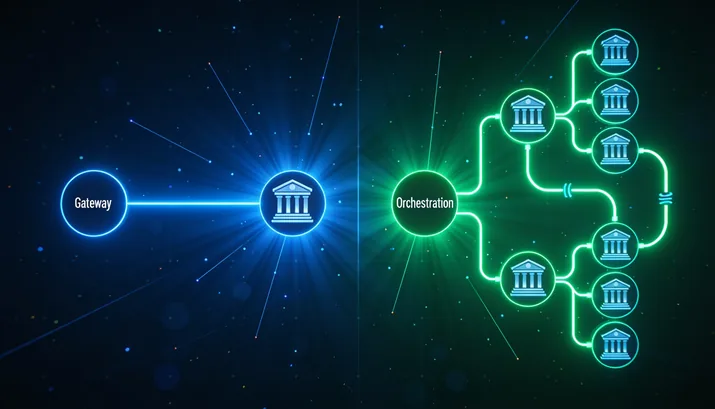

One bank, one market? You need a gateway. Add a second bank and you need orchestration — a layer that picks a bank for each payment.

Get this choice right and you spend less on integrations, win back sales you used to lose, and open new markets in days. Get it wrong and you either pay for routing you never use, or you outgrow one bank and feel it in your approval rate every day.

So the core question isn’t "gateway vs orchestration" in the abstract. It’s: do you want to outsource routing, or do you want to own it?

What this guide covers

- The two terms in plain words. A gateway is a single line between your checkout and one acquiring bank; orchestration sits above many connections and decides which bank handles each payment.

- Gateway vs orchestration, side by side. Both take a card and return an approval — they diverge the moment you have more than one bank, more than one country, or a decline you want to win back.

- When a gateway is the right answer. One market, one bank, healthy approval rate: a routing layer would have nothing to route. Fit comes before price.

- Choose orchestration if this is you. The signals are concrete: you run (or plan) more than one bank relationship — for approval rate, geographic coverage, or spreading risk.

- Most companies migrate, not choose. The usual path is to start on a gateway and put an orchestration layer in front of it when the cracks show — done in that order, the move is low-risk.

- Where Payneteasy fits. A bank-agnostic platform: the same single connection links the gateway you already have to every bank you add, with smart routing, decline cascading and a vault that is not chained to one bank.

First, the two terms in plain words

Let’s strip away the jargon.

Payment gateway

A payment gateway takes a card at checkout, encrypts the card details, asks one bank "can you approve this payment?", and then carries the result back to your store. It’s a single phone line between your business and one acquirer — the bank or processor that clears the payment.

Most businesses start here, and they should. One bank is enough to take your first payments in a single market with a single acquiring relationship.

Payment orchestration

Payment orchestration sits one floor up — as a smart routing layer above your gateways.

Instead of one phone line, it’s a switchboard:

wired to several gateways and banks,

connected to local payment methods and alternative rails,

all behind a single integration.

For every payment, orchestration applies rules like:

"Send this card BIN and currency to bank A."

"Send this card BIN and currency to bank A." "If bank A returns a soft decline, retry through bank B."

"If bank A returns a soft decline, retry through bank B." "Keep local payment methods on the local rail."

"Keep local payment methods on the local rail."

The gateway answers:

"Can this go through here?"

Orchestration answers:

"Where should this go, and what do we do if it fails?"

So calling gateways and orchestration "rivals" is a mistake. Orchestration uses gateways. The honest question is not "gateway or orchestration", it’s whether a single gateway should carry your whole business or whether you need a routing brain above several of them.

Gateway vs orchestration, side by side

Both take a card and return an approval code. They diverge as soon as you have more than one bank, more than one country, or a decline you want to win back. Think of the differences like this:

| Payment gateway | Payment orchestration |

|---|

| Acquirer connections | One acquirer / processor per integration | Many acquirers, gateways and APMs behind one API |

| Routing logic | Fixed; each transaction goes where that gateway is wired | Rule-based and dynamic; routes by BIN, currency, amount, MCC, success rate, region, etc. |

| Declines | Returned as-is to the merchant — a loss unless you manually retry | Soft declines can be cascaded to an alternate acquirer |

| Redundancy | If the acquirer is down, payments stop | Traffic fails over to a healthy acquirer automatically |

| Tokenisation | Vault usually tied to one provider | Provider-agnostic vault, so the same token works across multiple acquirers |

| Reconciliation | One settlement file, one format, per bank | Normalised reporting across all connected acquirers |

| Adding a market | A new integration project per acquirer | A configuration change on the existing API |

| Best fit | Single market, single acquirer, predictable volume | Multi-acquirer, multi-market, or growth that has outpaced one bank |

You can read that whole table as one sentence:

A gateway executes a routing decision someone already made; orchestration makes that decision on every single payment.

The further your business moves toward "many banks, many countries, many methods", the more that difference compounds into hard gains or hard losses.

When a payment gateway is the right answer

A single gateway is the right answer more often than orchestration vendors admit. Fit comes before price.

Pick a gateway if:

You sell in one market through one bank.

When all your volume clears the same acquirer in the same currency, a routing layer has nothing to route. You would be paying for options you never use.

Your approval rate is already healthy and steady.

If declines are low and your bank rarely has outages, cascading and failover solve a problem you don’t have yet.

You want the fewest moving parts.

One integration, one settlement file, one support contact. For an early-stage merchant, that simplicity is worth more than a marginal gain in approvals.

In this scenario, a solid gateway plus a strong acquiring relationship gives you a clean, maintainable stack.

Orchestration earns its place the moment one bank relationship stops being enough. The signals are concrete, not vague; you’ll recognise yourself in at least one:

| Signal | Why it points to orchestration |

|---|

| You run, or plan to run, more than one bank | The reasons are usually:- lift approval rate,

- expand geographic coverage,

- avoid putting all risk on one rail.

Once you have two banks, something has to decide between them for every payment. That something is orchestration. |

| You are losing recoverable money to declines | A real share of declines are soft — issuer timeouts, transient risk flags, temporary glitches. Cascading those soft declines to a second acquirer wins back sales a single gateway simply hands back as a loss. |

| You are growing into new markets | Local acquiring and local methods lift approvals and reduce cost, but each new provider is an integration. Orchestration turns "add a bank" into a routing rule instead of a multi-month project. |

| Reconciliation has become a tax | Every bank reports differently. When finance spends more time tidying settlement files than analysing them, a layer that normalises data across providers pays for itself. |

If any of these are true, you’ve outgrown "gateway only".

Most companies don’t choose on day one — they migrate

Here is the part that takes the pressure off the decision. Few companies pick between the two at the start. They begin with a gateway and add orchestration when the cracks show. Done in the right order, the move is low-risk.

1. Put the orchestration layer in front of the gateway you already have

Your current bank becomes the first route. Nothing about how payments clear changes yet. You have only moved the decision point.

→

2. Add a second bank and one routing rule

Start narrow — one card type, or one country. Watch the approval rate before you widen it.

→

3. Turn on cascading for soft declines

This is usually where the recovered money first shows up, and you can measure it against your pre-migration baseline.

One detail decides how clean the move is: the tokenisation vault — where your stored card numbers live. If that data sits inside a single gateway’s vault, "portable" tokens are portable only on paper. Moving them means migrating the raw card number, called the PAN — the full 16-digit account number — and re-tokenising everything, which is slow, sensitive work. A provider-agnostic vault, or network tokens you control, is what keeps banks swappable instead of sticky. Settle that before the second bank, not after.

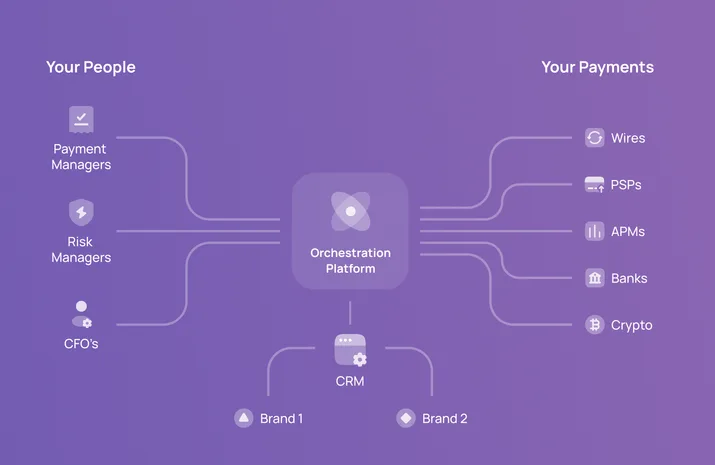

Where Payneteasy fits

Payneteasy is built bank-agnostic, and that is the point of this whole piece.

The same single connection links the gateway you already have to every bank you add afterwards.

Smart routing and cascading decide which acquirer each transaction goes to, and what happens on a soft decline.

A provider-agnostic vault and PCI DSS Level 1 infrastructure keep stored cards from being chained to one bank.

You don’t have to pick a side today:

Today: your gateway

If you’re still on one bank, Payneteasy can run as your gateway.

→

Tomorrow: your orchestration layer

The day you add a second bank, the same integration becomes your orchestration layer, with no re-integration to slow you down.

Because it’s available white-label, PSPs and platforms can offer that routing intelligence under their own brand:

Your brand in front

Your merchants see your name on the gateway and checkout.

→

Payneteasy behind it

Payneteasy provides the multi-acquirer routing, cascading and vault behind it.

If you want help mapping "gateway vs orchestration" to your own numbers — bank count, markets, methods — Payneteasy’s team can walk it with you before you commit.