How to Choose a White-Label Payment Gateway Provider

Pick a white-label payment gateway provider whose gateway runs under your brand, launches in 2–4 weeks, and lets AI safely read your payment data.

03.07.2026

12 min read

Meet us at conferences around the world

iGB L!VE London

SBC Summit Lisbon

SiGMA Europe

Pick a white-label payment gateway provider whose gateway runs under your brand, launches in 2–4 weeks, and lets AI safely read your payment data.

Selecting a white-label payment gateway provider is one of the highest-stakes infrastructure decisions a payment business makes: the wrong choice ends in an expensive migration; the right one becomes an asset that renews and expands with your brand for years.

You are not buying "software." You are buying the ability to run a payment business that your customers associate with you, not with the vendor. Judge providers on outcomes: what you own, how fast you can bill, and how safely you can let AI read your operational data.

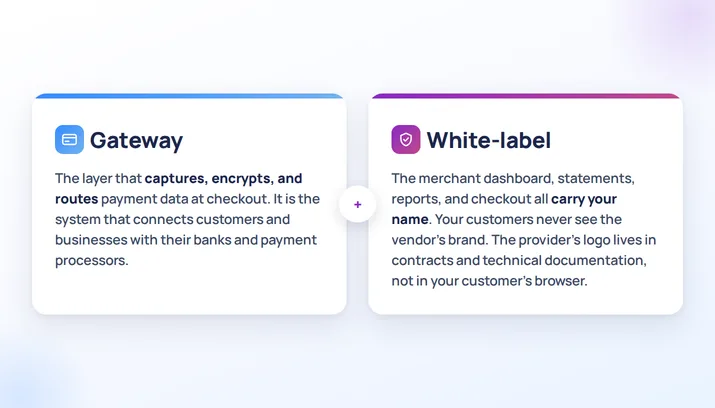

Let me define two words up front. A "gateway" is the layer that captures, encrypts, and routes payment data at checkout. "White-label" means the dashboard your merchants log into, the statements they read, and the checkout they integrate all carry your name. The vendor's name appears nowhere your customers can see.

That distinction sounds cosmetic. It is not. It is the difference between reselling someone else's product on their roadmap and running an asset that renews with you. Keep that frame as you read on. Every criterion below either protects that ownership or quietly hands it back to the vendor.

Payneteasy's model is genuinely white-label:

This directly addresses the first pain many ISOs, PSPs and platforms feel with other providers: they invest in sales and support, only to see the vendor's name take the loyalty and referrals. With Payneteasy, that asset accrues to you.

Most selection processes begin with a feature matrix and end with a compromise. That is backwards.

You should start from a small set of business decisions:

Treat the feature grid as evidence for those decisions, not as the verdict. A clean architecture diagram and a clear go-live path tell you more about risk and revenue than any marketing checklist.

Payneteasy is structured to win on both:

1) Brand ownership: You stay the face of the business. Merchants see your logo, your domain, your communication. Payneteasy is the engine and back-office, not the storefront. That solves the "ghost brand" problem where your vendor becomes more visible than you.

2) Time to live: Payneteasy typically gets you live in 2–4 weeks. You configure routes, projects, endpoints and branding instead of spending quarters building infrastructure. That short window directly addresses the pain of slow launches: every week shaved off implementation is a week of revenue brought forward and a deal saved from a faster competitor.

When a buyer asks "how long until I can invoice my first merchant under my own brand?", Payneteasy's answer is measured in weeks, not quarters — and that is where it closes the gap most platforms feel with home-grown stacks or heavier vendors.

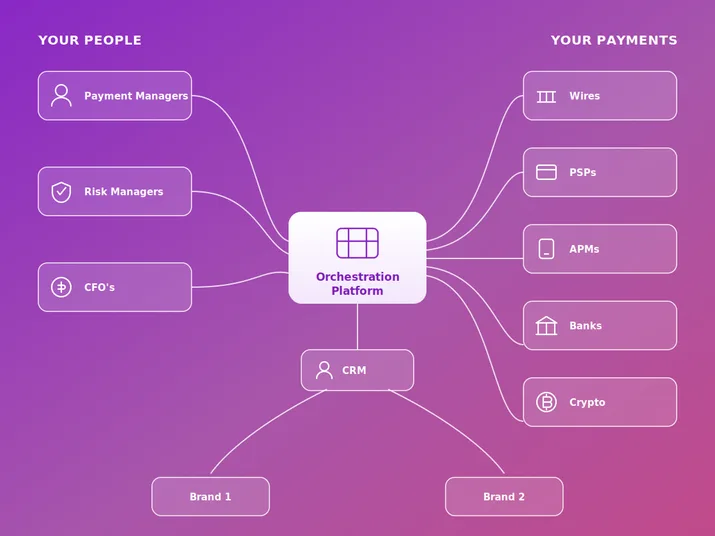

Branding sits on top of the part that actually makes money. That part is routing. In a modern payment stack:

On top of an OpenAPI-described processing API, routing and cascading give you three concrete advantages:

Payneteasy's orchestration runs on a Processing API described in OpenAPI 3.1 and gives you:

One honest caveat that also protects you: Payneteasy routes across the bank and provider relationships you already hold. It is not a PayFac or acquirer. You bring and keep your acquiring; Payneteasy's job is to make those contracts work harder through better routing. That separation addresses the fear many PSPs and ISOs have that a "platform" will quietly become their competitor.

For years, the white-label choice hinged on two axes: brand control and integration depth. A third axis has arrived: safe AI-grade observability of operational data.

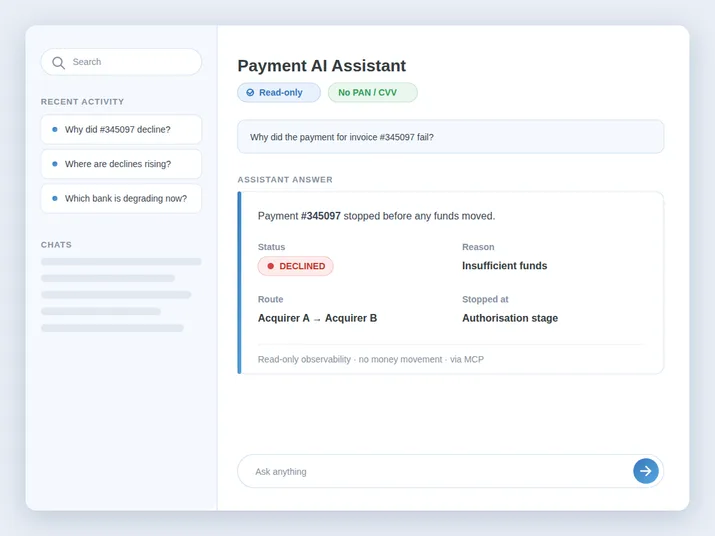

Inside most payment businesses, the demand already exists. Teams paste transaction IDs, error codes and spreadsheet exports into assistants like ChatGPT, Claude or Copilot and ask questions like "why did this batch fail?" or "where are declines concentrating this week?" Founders want agents that reconcile settlements; support leads want agents that explain declines before merchants churn.

The usual workaround is dangerous. To give an AI tool access, teams hand it a database password or an API key that can both read and move money. From a security and compliance standpoint, this is precisely the access a risk team should never approve. Read access and money movement are not the same key. Architecturally, they should never travel together.

Payneteasy closes that gap with a read-only MCP server:

That architecture directly addresses two growing pains:

Most competitors do not have an answer here. Payneteasy's MCP layer gives you a clean, defensible story when a customer asks "why you, not the incumbent?" — especially if that customer is already pushing for AI-grade transparency.

Score every provider against criteria that map to revenue and risk, not a feature grid. Run down this list on your next call.

The row most competitors cannot credibly fill is the AI-agent one paired with a hard architectural boundary around money movement. If a provider cannot show you that line on an architecture diagram, not just in a brochure, it does not exist.

| Criterion | What to ask |

|---|---|

| Brand ownership | Is it truly your gateway, or their product with your logo on it? Do merchants ever see the vendor's name in the dashboard, checkout domain, emails or statements? |

| Time to live | Are you looking at weeks of configuration or at a multi-quarter engineering project? How many weeks of unbilled revenue are hidden inside the implementation plan? |

| Routing control | Can you author and maintain your own routing and cascading rules across multiple providers and banks? Or are you locked into vendor defaults and opaque decision trees? |

| AI-agent access | Can AI assistants observe your operational data safely through a read-only interface? Or is "AI access" possible only via credentials that could also move money? |

| Money-movement boundary | Is the separation between read access and write/settlement enforced in the architecture? Or is it simply promised in a contract and left to best effort? |

| Track record | How long has the platform processed real volume under real load and regulatory scrutiny? Is there evidence of surviving high-stress scenarios before yours? |

Platforms serving high-risk or tightly regulated categories — gaming, gambling, lending, global marketplaces, subscription SaaS — need routing that survives declines and respects each bank's rules without handing their merchant base to the technology supplier.

Payneteasy's core combination of broad provider coverage, smart routing, cascading, and AI-ready observability addresses that:

For a head of payments, that combination — survivable routing plus safe observability plus a non-competing provider role — is what closes the risk gap that often blocks adoption of "new" platforms.

If payment routing infrastructure is your product and you have the engineers and years to invest, building your own engine can make sense. You will own every line of code and every operational risk.

For most PSPs, platforms and large merchants, the trade-off looks different:

Building means multi-quarter timelines, high opportunity cost, and the responsibility to maintain a complex engine for a decade.

Buying Payneteasy means trading that engineering effort for:

Payneteasy is explicitly designed to be the "buy" option that does not cost you ownership: you give up building the engine, but you keep the business that runs on top of it — brand, bank relationships, routing strategy — and gain an AI-ready view that most incumbents cannot offer.

A white-label payment gateway provider supplies the gateway technology you operate under your own brand, so your merchants see your name across checkout, dashboards, and statements. The strongest providers also give you control over routing and integration rather than a fixed product. Payneteasy lets you launch a branded gateway in 2–4 weeks.

It means assistants like ChatGPT, Claude, or Copilot can read your live payment data through a safe, structured interface. Payneteasy provides this with a read-only MCP server: agents observe payments and routing state and can never move money. Teams get AI for analysis and reconciliation without widening their PCI or fraud exposure.

No. The MCP server is read-only observability by design, so agents can read payment and routing data but cannot start, change, or move a payment. Money movement runs through a separate Processing API governed by your own systems and rules. That separation is the security guarantee, not a setting you have to switch on.

Payneteasy launches a white-label payment gateway in 2–4 weeks under your own brand. The speed comes from running on an established platform instead of building processing infrastructure yourself, so your go-to-market is measured in weeks of configuration, not quarters of engineering.

Thank you for reaching us. Your request has been sent successfully. We will get back to you as soon as possible.

Message was not sent